The S&P 500 is sitting at 6,582. It’s down 4.6% to start 2026, but analysts are still calling a soft landing. Nobody seems to be panicking. Yet, the Fed is still trapped by its own dual mandate, trying to juggle high inflation and unemployment through interest rates, and Brent Crude Oil swung from $110 a barrel to briefly below $90 before a false ceasefire signal, only to climb back toward $98. We are quick to dismiss a very real possibility: the return of stagflation similar to that in the 1970s.

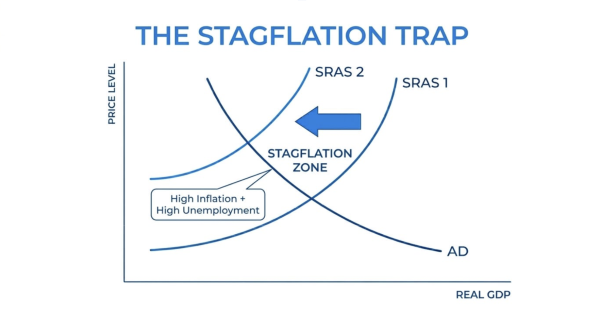

In my AP Macroeconomics class, stagflation is seen through the leftward shift of the Short-Run Aggregate Supply Curve.

In the 1970s, we struggled with the same issues we are dealing with right now: high oil prices and recessionary output gaps caused by conflict in the Middle East (the Iranian Revolution at the time).

Each day the Strait of Hormuz is shut, oil prices skyrocket just a little bit more. But even if the Strait were to be opened tomorrow, it would take months to stabilize oil prices for two primary reasons.

- A disruption in global supply chains takes a long time to restabilize due to the nature of its complexity.

- Markets are based on perception. If a higher level of risk is deemed to be associated with oil, it takes a long time to reestablish stability.

The Fed is trapped and can’t cut interest rates since that runs the risk of spurring investment, and therefore raising inflation rates—a risk that the US can’t afford to make.

I asked AP Macroeconomics teacher Mrs. McKie whether the Fed has more tools available than people realize. She told me, “The Fed is trying to keep its options open, but those options are fairly limited. In his most recent speech, Chair Powell repeatedly emphasized ‘uncertainty,’ reflecting the current situation. By choosing not to change interest rates, the Fed is essentially buying time—waiting to see which side of its dual mandate, inflation or unemployment, becomes the more pressing concern.”

The competing pressures and factors make waiting uncomfortable. As Mrs. McKie explained, ongoing conflict in the Middle East could lead to inflation, which would ultimately call for higher interest rates. At the same time, uncertainty about long-term AI effects persists, and ultimately, the Fed is stuck between raising rates and trying to stabilize an already stressed economy.

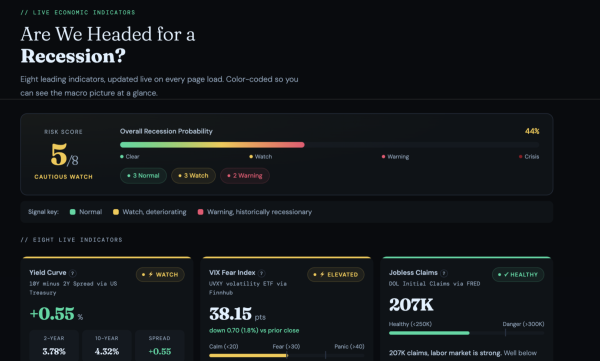

The Recession Dashboard

There are a few economic indicators I use to track our stability and to maintain my level of worry. I used Claude to create my own indicator dashboard, which I linked below.

Definitions of each indicator

Copper: It’s used in everything from buildings to electronics. Once demand falls, it’s not a good sign (investor/business pessimism). In my opinion, it is one of the most reliable leading indicators of a recession.

One may look at today’s graph and see rising copper prices, yet the current rally is tariff/AI-driven, not driven by real demand.

The Buffett Indicator: The total stock market value divided by GDP. Buffett called it the best single measure of whether stocks are cheap or expensive relative to the actual economy, and if the economy is overvalued.

Jobless Claims: The number of people who filed for unemployment insurance in the past week.

I find this to be both a lagging and a leading indicator, as companies that fear recessions will preemptively let go of employees, but it also tracks the number of people unemployed following/during a recession.

VIX (Volatility Index): This is Wall Street’s anxiety meter. A higher index is no sign of anything good.

S&P 500 vs. 200-Day Moving Average: The S&P 500 versus its long-term trend line, which I believe is one of the most important lagging indicators. And given that optimism is a self-fulfilling prophecy, a lower S&P below the trendline is a strong sign of a bear market.

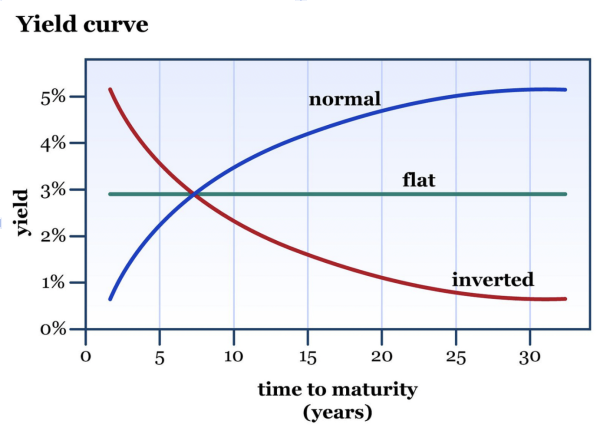

Yield Curve: The graph of yields on (typically) Treasury bonds, and if short-term bonds pay more than long-term bonds, the market may be signaling a possible recession.

- An inverted curve can be a sign of a recession.

- An upward-sloping curve is a sign of a healthy economy.

High-Yield Spreads: If a business is deemed more risky (“junk” bonds), investors will demand higher interest rates. The spread is the yield relative to the benchmark (usually US Treasuries), and a reliable leading indicator of recession is when the spread increases or widens. In other words, the price of interest rates for junk bonds increases relative to the perceived risk of those bonds.

Brent Crude Oil: Our entire global economy relies on oil, and a spike in prices leads to a plethora of issues. One of which could be stagnant growth and stagflation, just as we saw in the 1970s.

What does this mean?

The Fed is essentially trapped. They can’t cut rates without raising inflation, and they can’t raise rates without slowing an already declining economy.

The indicators aren’t screaming recession yet. Jobless claims are healthy, and credit spreads are still tight. But the Buffett Indicator is at around 232%, the S&P 500 is hitting 52-week highs, and oil is surging for reasons that won’t resolve overnight. Not to mention the yield curve just re-steepened after two years of inversion, which historically is the most dangerous moment, as we’ve seen during the Dot-Com crash, the 2008 Financial Crisis, and the months before COVID.

There are also risks that many people haven’t focused enough on yet. The first is China and its reliance on oil. Mrs. McKie explained, “The impact of this oil crisis on a major global power like China, which relies heavily on oil imports from the Middle East, much of this oil passes through the Strait of Hormuz. We should be thinking carefully about how Chinese leadership might respond…if energy prices rise significantly, how will the Chinese public react, given the implicit expectation of economic stability?”

The second is the global food supply. A significant portion of fertilizer used, especially in the US, moves through the Strait. Prolonged closure could mean amplifying food insecurity, especially in vulnerable areas such as South Asia, East Africa, and some parts of Latin America.

My prediction

The most likely outcome is not a crash but a slow squeeze on the economy into higher inflation and lower real income, driven by sticky wages.

For a brief moment around April 17th, Iran declared the Strait open, and consequently, oil prices dropped 10%. Yet by Saturday morning, April 18th, the IRGC (Islamic Revolutionary Guard Corps) had reversed it, and the Strait was closed again.

As Mrs. McKie put it, “There is still some hope that this situation will be resolved sooner rather than later, though that optimism is limited. The stakes are quite high, particularly given the political implications for control of the House and Senate. Because of that, there will likely be strong incentives for policymakers to take action to reduce inflationary pressures and find a viable exit strategy.”

The wildcard is the issue of the Strait of Hormuz. If it reopens permanently within the next 60 days, oil can normalize by summer, and most of this should resolve in the near future. If it stays closed through the summer, $130+ for Crude oil becomes a realistic possibility, and the global economy digs itself into a deeper hole.

TL;DR

The Strait of Hormuz has been effectively closed since late February, and briefly reopened for about 24 hours on April 17th before Iran reversed it. Oil is back around $98 a barrel. The Fed can’t cut rates without making inflation worse. The eight recession indicators I have above are flashing between watch and warning, and as Mrs. McKie put it, “a resolution is possible, but far from guaranteed.” The economy looks fine on paper, but right now, the price of oil is being set by geopolitics, not supply and demand.

- Stagflation: the slow growth of a country’s demand tied with high unemployment and inflation rates.

- Soft Landing: A slowing of growth through higher interest rates to avoid a recession.

- Sticky Wages: The idea that during inflation, real income decreases because contracts are fixed, and due to the fact that most wages don’t adjust to inflation.

Thanks to AP Macroeconomics teacher Mrs. McKie for sharing her perspective.